COVID-19 impact could take 5 years to be fully understood: survey results

The results of the second COVID-19 survey by Reinsurance News suggest that it may take up to five years to fully understand the impact that the pandemic will have on the insurance and reinsurance markets.

The survey, undertaken in collaboration with ILS focused sister-site Artemis, acted as a follow-up to our April survey, which sought to take the pulse of the global reinsurance market at this unprecedented and challenging time.

The survey, undertaken in collaboration with ILS focused sister-site Artemis, acted as a follow-up to our April survey, which sought to take the pulse of the global reinsurance market at this unprecedented and challenging time.

Now two months on, with COVID-19 still profoundly impacting the market, our latest survey aims to show how re/insurers’ views of the crisis have changed, while also providing fresh insights.

The new COVID-19 Market Survey includes responses from hundreds of identifiable market participants, of which more than half have responsibility for, or provide input to, reinsurance and retrocession buying decisions.

This includes 16 CEO’s, 15 CUO’s, 12 COO’s, 27 senior Board members, reinsurance buyers, senior underwriting executives, ILS managers, brokers and a range of service providers.

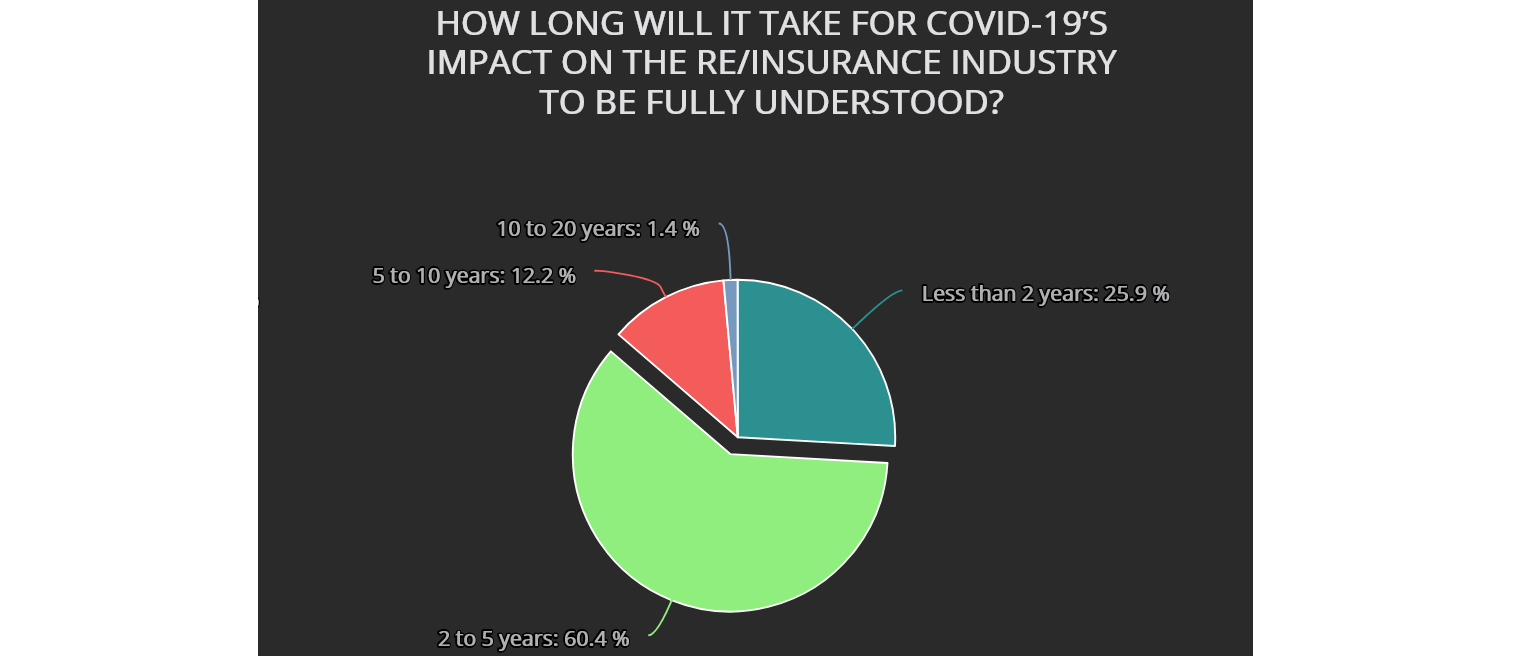

While 25.9% of these respondents were hopeful that the full impact of the pandemic could be understood in less than two years, 60.4% agreed that it could take up to five years.

There was broad consensus in other areas too, as the majority of survey answers indicated that re/insurers are more concerned about the affect of COVID-19 on the underwriting side of their business, rather than on the investment side.

And in terms of underwriting losses, the vast majority (85.3%) saw non-life business as more exposed than life business.

There were mixed thoughts about the overall size of the industry’s non-life underwriting loss, although the $80-100 billion range proved the most popular, with 27.3% of respondents favouring this option.

The adjacent ranges of $50-80 billion and $100-150 billion were selected by 14.4% and 20.1% of respondents, respectively, and the top end of $200+ billion also came in at 14.4%.

With opinion split across such a wide range of potential loss scenarios, it seems to reinforce the sense that it could be a number of years before the market is truly able to put a concrete figure on the cost of the pandemic.

Also supporting this notion was the general agreement that the highest levels of pandemic losses are yet to be reported, as roughly a quarter of respondents felt that the highest levels of claims would be seen in the second quarter of the year, while 39.6% forecast the highest losses in Q3, and 19.4% in Q4, with others putting the heaviest impact even into 2021 and 2022.

Other questions offered insight into the market’s view on legal efforts surrounding retrospective business interruption claims, which less than 15% of participants now feel is likely to be successful.

This compares to the results of our previous survey, when almost one third of respondents said they were very concerned, while almost 18% said they were extremely concerned.

But more than two-thirds of respondents to the latest survey said they anticipate ‘significant changes’ to business interruption policies following the pandemic.

And there was also broad consensus that government supported backstop reinsurance schemes for future pandemics should be implemented, with 22.3% classing them as essential, 41.7% as definitely helpful, and 28.8% saying they would help a bit.

What is clear from the survey results is that there remains a tremendous amount of worry and uncertainty when it comes to unprecedented challenges that the market now faces.

Amid all of this uncertainty, we hope that this survey can help to capture a snapshot of this historic moment, create useful data to inform actions, and take the pulse of the market at this time.